Graph 1.six

Sources: ECB, Bloomberg Loans L.P., European Commission and you may ECB calculations.Notes: Committee a: interest rate sensitiveness is calculated since market beta of business EURO STOXX sub-list towards the German five-seasons authorities bond along the several months out of . Expected CAPEX reflects Bloomberg’s imagine of the amount of cash an excellent organization spends to acquire financial support possessions or inform their present investment property. A negative value reflects higher expense. Committee b: practical departure across 56 NACE Rev. 2 groups about euro urban area.

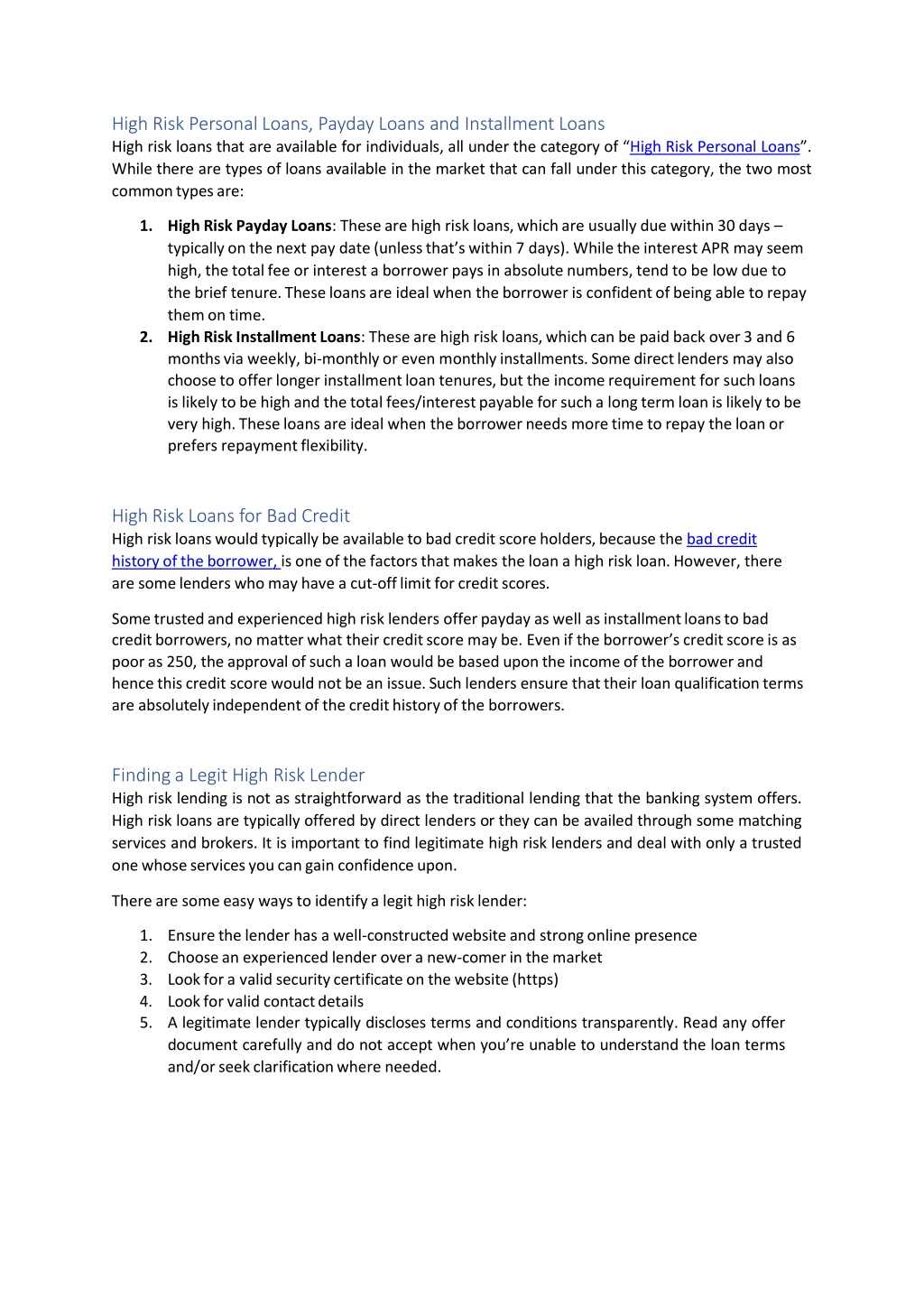

Firmer funding criteria have begun to own an effect on firms’ obligations solution will set you back and issuance habits. While the financial criteria provides fasten, both locations and you may banking companies possess reassessed the risks related corporate interest. Thus, the cost of obligations has increased dramatically given that middle-2022 (Graph 1.seven, panel an effective). Internet credit flows decrease right back firmly in the first months from 2023 whilst became more pricey so you’re able to roll-over personal debt, exhibiting deleveraging in a few nations and circles. Inside the 2022 large rates and higher working-capital means towards membership out-of high production will cost you in addition to triggered a move away from long-label credit to financing which have a smaller maturity. The outcome of your ECB’s Q1 2023 bank financing survey suggest that the escalation in the general amount of interest levels, plus a pencil need for the brand new credit. In addition, the brand new impression off tighter credit conditions you will build over the years, having a defer admission-up until the actual passion off businesses. In some euro city places, higher obligations solution need is actually followed closely by all the way down attract visibility ratios, and you will corporates was influenced a great deal more because of the ascending speed ecosystem.

Meanwhile, corporate balance sheet sets in the most common euro town places are currently more powerful than simply they certainly were during previous speed-walking time periods. Years from low interest rates and you may a powerful article-pandemic data recovery possess assisted the average business to build resilience during the that person away from a special downturn and you can rapidly rising capital can cost you. Terrible desire exposure rates features increased, particularly for nations hence become which have low levels of interest visibility on the non-financial corporate business (Graph 1.7, panel b). Also, non-financial corporate personal debt profile rejected so you can 144% from disgusting value added on the last one-fourth of 2022, compared with 148% until the pandemic.

Chart 1.seven

Corporates provides created strength, however, credit costs are increasing firmly and you can bankruptcies enjoys acquired in a few euro area nations

Moody’s Statistics, Refinitiv and you may ECB computations.Notes: Committee b: the debt services proportion is described as the fresh ratio of great interest costs and amortisations to money. Therefore, it offers a beat-to-move assessment the newest flow regarding loans provider costs separated of the circulate off income.* The attention coverage proportion is understood to be the ratio regarding terrible operating surplus to terrible appeal costs before the calculation out of monetary intermediation functions ultimately counted.*) Select How much money can be used getting debt repayments? An alternative database getting loans solution rates, BIS Every quarter Opinion, Bank getting In the world Agreements, .

Bankruptcies in a few euro town nations have started to boost of a highly reasonable feet, despite the fact that continue to be lower than pre-pandemic levels. Bankruptcies for the majority high euro city economies are still below pre-pandemic averages, while they have now reach normalise on the low levels hit in pandemic. Additionally, forward-appearing procedures to have standard risk laws raised risk (Chart 1.7, panel c), motivated of the those groups directly affected by the energy crisis such as for instance as transportation and you can globe.

Corporate vulnerabilities could well bad credit personal loans Washington be greater than the newest aggregate suggests, because the not every business benefited similarly on the blog post-pandemic data recovery. The fresh rough perception away from two thriving, and you can distinctly other, crises features big variety across the cross-section of companies and may mean that a financial market meltdown you’ll do have more major consequences to own financial balance than simply it aggregate image suggests. Additionally, brand new predominance out of changeable-rates credit in a few nations, as well as high corporate obligations levels because of the historic and you will worldwide requirements, renders particular corporates susceptible to a deeper otherwise crazy firming off economic standards. Moreover, loans devices that are way more responsive to rates develops, including leveraged money, might possibly be such started is monetary standards tighten further. Therefore, there can be significantly more non-payments going forward, that have possible knock-on the consequences towards the bank balance sheets and you will house a position applicants.