Would it be far better score good HELOC otherwise play with playing cards?

In the par value, HELOC vs. mastercard is not a fair endeavor. Household guarantee credit lines (HELOCs) are one of the cheapest types of credit while you are playing cards are among the most high-priced.

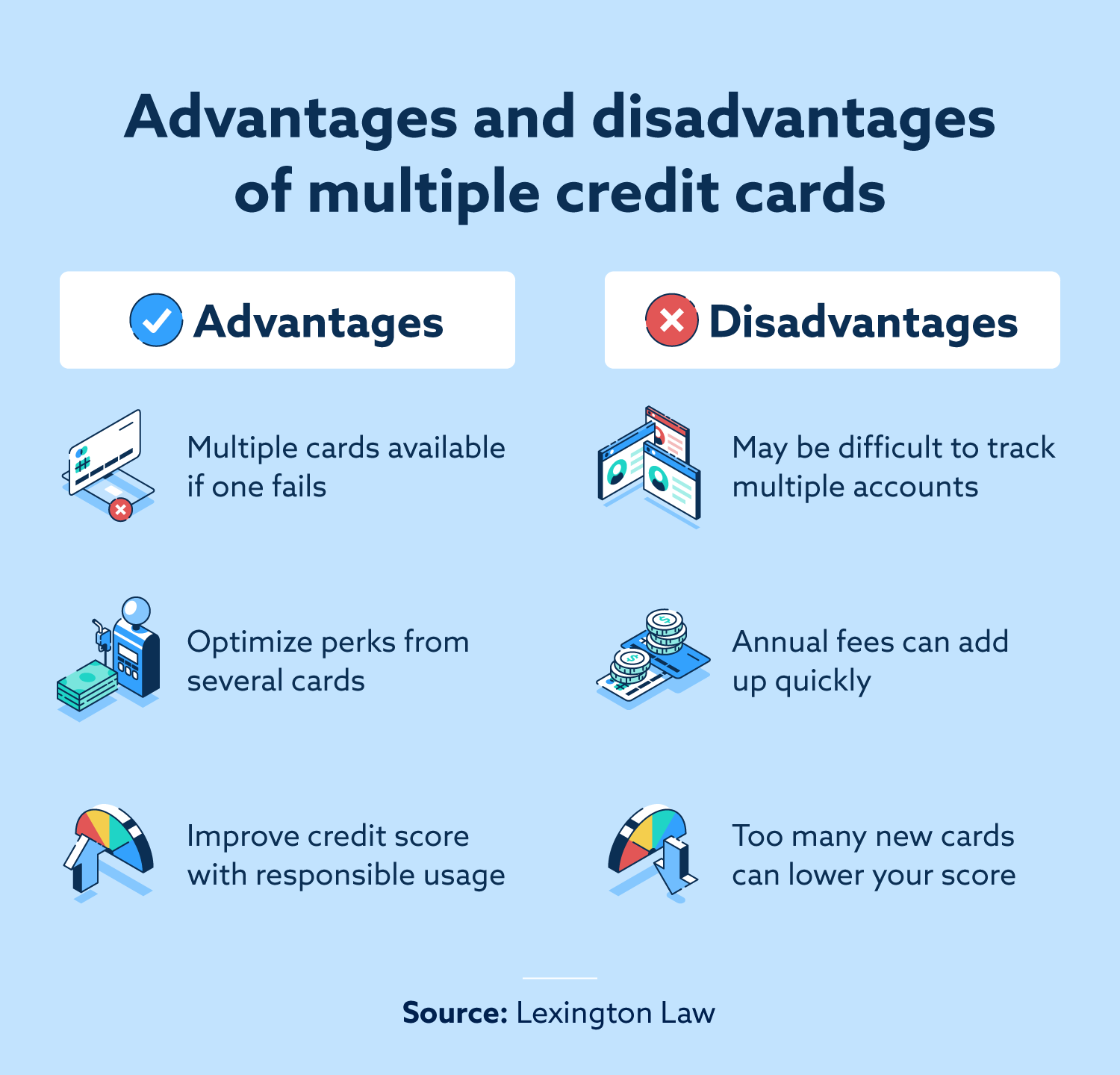

not, all sorts out of borrowing features its own advantages and disadvantages. So there are a couple of activities whenever charging credit cards try an effective wiser choices than tapping home security. Very continue reading to discover which are often a much better fits for your requirements.

HELOC against. bank card assessment

HELOCs and you can handmade cards vary financing items naturally. A great HELOC was an excellent shielded loan you to borrows from the offered household equity, while a charge card try an unsecured personal line of credit (meaning there is absolutely no collateral so you can back it up).

Both HELOCs and you can cards is actually credit lines. That means you will be provided a borrowing limit and can borrow, pay back, and re also-obtain normally as you wish doing the newest restrict. And also you spend notice just on your current equilibrium.

Both situations come having changeable pricing, definition their attention will cost you normally increase or fall in range having sector trend. However, of numerous HELOC loan providers enables you to secure the rate with the some otherwise your harmony whereas credit card pricing generally dont getting fixed.

Whenever is good HELOC top?

A property security credit line is typically a lot better than an effective bank card if you wish to borrow a large amount of currency and you will pay it back over a long period.

- You desire a top credit limit. Particular HELOC lenders offer the very least HELOC regarding $10,000 and others state $35,000. The utmost would be $one million or higher

- Need straight down rates of interest

- Is a beneficial creditworthy resident

- Have sufficient household guarantee to help you be eligible for good HELOC

- Wanted the possibility to lock the pace for the certain or all of one’s equilibrium (only a few loan providers let this)

- Need certainly to cover your credit score throughout the outcomes of overusing playing cards

If you’re able to have one, an excellent HELOC often typically overcome a charge card. You can study much more about what’s expected to be eligible for a HELOC right here.

Whenever try handmade cards better?

- Won’t need to use a large amount. Credit cards is better having short, day-to-day costs

- Are unable to score an effective HELOC and other economical kind of mortgage or line of credit

- Has a temporary crisis and require quick capital

It’s normally better to avoid handmade cards having big expenses instance domestic home improvements otherwise carrying out a business. But for regular, day-to-big date using, handmade cards make sense and will offer perks (such as for example take a trip perks).

What is the difference in a HELOC and you can credit cards?

No matter if HELOCs and you will playing cards operate in the same means, you can find extreme differences when considering both. This is what to adopt because you weighing https://paydayloanalabama.com/rock-creek/ the benefits and you can drawbacks:

Protected compared to. unsecured borrowing

Playing cards is actually unsecured borrowing. That means you’re not setting up a secured asset as the defense (collateral) on the financing. If you’re unable to pay back that which you borrow, there is absolutely no lead way for their bank to grab certainly the possessions.

HELOCs, however, is actually a type of next home loan. That implies these include safeguarded by your domestic. Very, for people who slide far adequate behind along with your repayments, you can face foreclosures.

In addition form HELOCs appear merely to people. No domestic function no guarantee which zero HELOC. Therefore, when you’re among around thirty-six% of property which lease their houses, you will need to move to cards, unsecured loans or some other style of borrowing from the bank. Discover a listing of alternatives lower than.