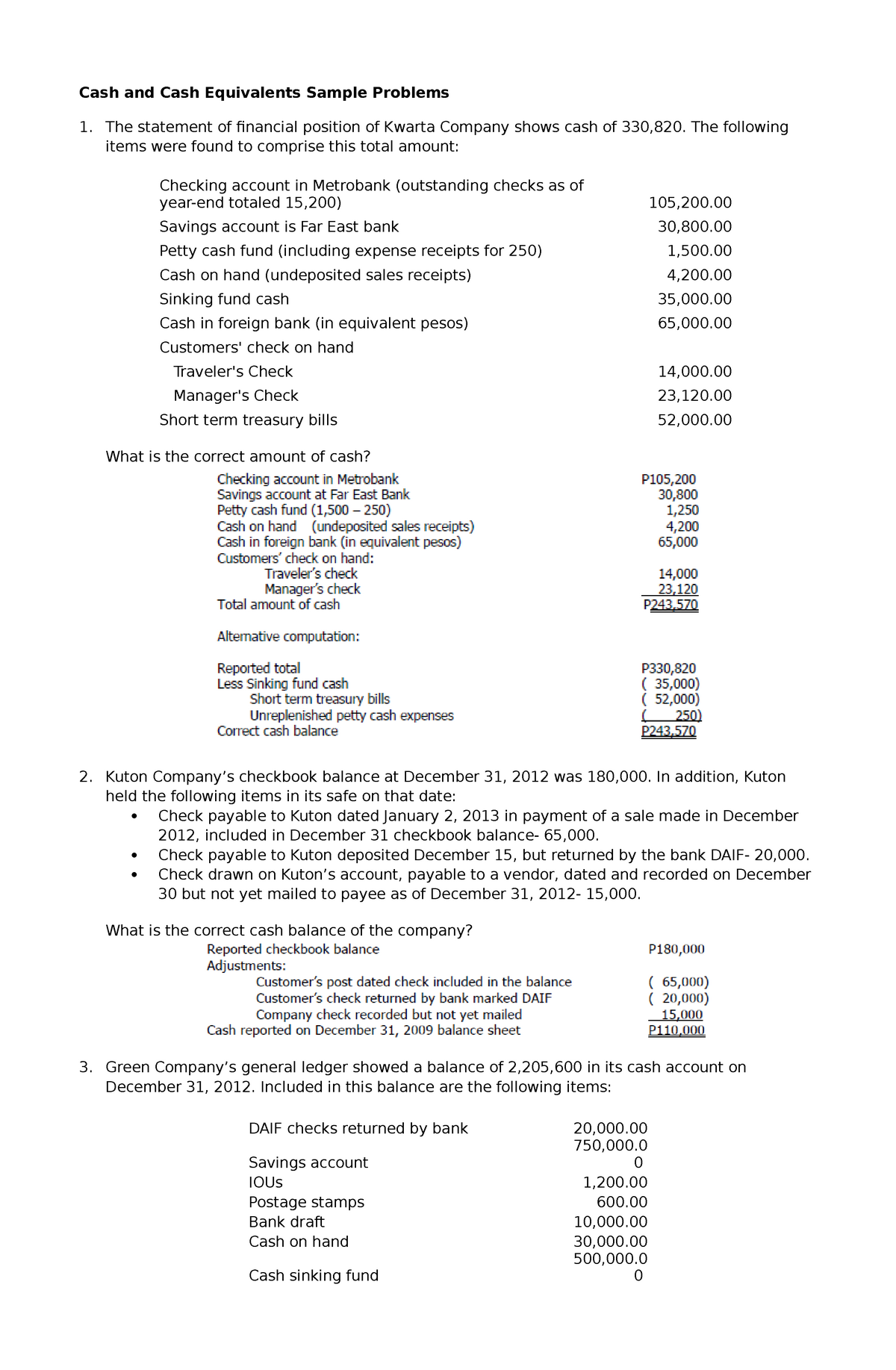

Truth be told: Delivering acknowledged getting a normal loan can be problematic, specifically for lower- to modest-income homebuyers with shorter-than-prime borrowing from the bank. not, antique finance have numerous pros. For starters, this loan form of generally also provides much more aggressive interest rates and better financing limitations. Financial insurance is also a consideration. Whereas very FHA loans require PMI, old-fashioned fund simply need it for many who place less than 20% off.

FHA otherwise Traditional Loan? That’s Best?

Regardless if you are an initial-date home visitors or a bona-fide house master, it’s also possible to wonder: What exactly is best an FHA financing within the Virginia otherwise a normal loan? At the Dashboard, our very own Home loan Teachers are faced with which concern daily. We constantly tell homebuyers that it depends. When you have a lowered FICO* get and you will limited cash, a keen FHA loan could work. Although not, in case the credit rating exceeds 640 along with adequate bucks having a much bigger down-payment, a traditional financing is better for you.

Still being unsure of which financing choice is just the right complement? Contact Dashboard on the web otherwise call 757-280-1994 to connect which have a home loan Advisor.

Antique Loan Restrictions to possess Virginia Borrowers

The quantity you could potentially borrow is decided because of the financial. Although not, there are also even more restrictions. Simply how much you could acquire hinges on their creditworthiness, debt-to-money proportion, or other factors. However, private lenders must conform to conditions put by Federal Construction Money Agency. This new conforming financing maximum to own 2023 is $726,two hundred for the majority of elements. In certain higher-buck a house parts, borrowers could possibly get recognized to own loans around $1,089,3 hundred.

- Your meet up with the credit history conditions. The minimum credit score vary out of bank so you’re able to bank; but not, most loan providers predict a beneficial FICO* rating with a minimum of 680. Dash now offers traditional finance to help you consumers with results only 620. Only keep in mind that homebuyers that have a score over 740 get the very best costs.

- You have got a fair obligations-to-money ratio. Your debt-to-earnings ratio try determined because of the separating complete month-to-month financial obligation payments by the month-to-month gross income. Very loan providers want to see a financial obligation-to-income ratio of about 36%.

- Zero big credit file activities, such as for instance a property foreclosure otherwise bankruptcy proceeding.

- A down payment with a minimum of 3%. If not must pay PMI, you will have to set out 20% of loan amount.

Particular Conventional Fund having Virginia Home buyers

Conventional lenders are like popsicles they show up in lot of other tastes. Each kind off antique mortgage is perfect for individuals with various other demands. Unsure which is for your requirements?

Browse the traditional fund we provide, following get in touch with home financing Mentor at Dash.

Just like Mike Krzyzewski, your Home loan Coach is here to be certain the financing process is actually an effective slam dunk. They may be able address every inquiries you have got regarding the traditional financing inside the Virginia.

- Conforming Antique Financing: Match requirements place by Government Construction Finance Department.

- Non-Compliant Traditional Mortgage: Cannot satisfy requirements place of the Government Housing Loans Company.

- Virginia Jumbo Financing: A type of nonconforming antique financing you to exceeds simple financing limitations.

- Fixed-Rate Loan: Old-fashioned loan option which have fixed rates of interest.

- Adjustable-Rate Financing: Designed for individuals which acceptance upcoming develops inside the earnings.

Ideas on how to Get a normal Mortgage inside the Virginia

To try to get a traditional loan, you’ll need to fill out an application exhibiting your earnings, credit history, and all sorts of property, including bucks, later years assets, plus life insurance. Mortgage lenders also want to make sure you possess multiple months’ value of mortgage payments on your family savings in case there is an urgent situation.